As FX volatility grows, treasurers must reexamine company exposures to defend or improve their FX management strategy.

The rise of the dollar over the recent weeks has, without a doubt, created tremendous turmoil within treasury departments around the world. Even when trends have been long-anticipated, such as the euro devaluation, it is impossible to predict the exact timing and magnitude of these macro corrections. Before the US dollar strengthening, we saw currency wars among major economies in Asia, and currency devaluations in Latin America. Global company treasurers are experts in managing currency risk, but they can only manage the exposures known to them. So it’s especially important to reevaluate those exposures during times of increased volatility when even a small forecast variance can result in big currency-related losses.

Start by measuring transactional exposure

Whether or not you hedge your transactional exposure, it is fundamental to measure the company’s sensitivity to currency rate fluctuations on foreign currency sales and purchases.

There are two schools of thought about hedging transactional exposure. The first one, the hedging approach, tends to favor protecting known exposures and smooth the effect of currency volatility, at least in the short-term. The second one, the market approach, favors leaving these cash-flows un-hedged because hedging short-term volatility is expensive and futile knowing that the long-term trend can’t be hedged anyway. Regardless which school of thought you favor, understanding your exposure is essential.

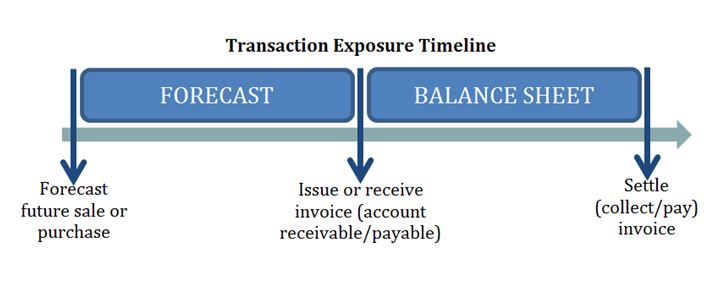

Transaction exposure as illustrated in the timeline diagram below is composed of two parts: “forecast” and “balance sheet.” Companies typically measure each part independently.

Capturing balance sheet exposure is relatively easy

The evolution of FX management in global companies often begins by measuring—and hedging—balance sheet exposures. After all, these assets and liabilities, subject to revaluation, are known exposures and are relatively easy to measure, sometimes even centrally if you are lucky enough to have a global accounting system. Hedging balance sheet exposures is also relatively easy with rolling monthly or quarterly forward contracts, typically matching the whole value of the underlying exposure it tries to hedge. Even accounting for balance sheet hedge contracts is straightforward. The benefit of hedging your balance sheet is widely recognised as it reduces income statement volatility. The majority of companies agree that balance sheet hedging makes sense and they accept it as a routine part of currency management.

The best cash-flow forecasts come directly from the operating unit financial controller

While balance sheet exposure identification is well developed in most companies, identifying the forecasted portion of the same transaction exposure is not as common. These forecasted or anticipated foreign currency cash-flows have not yet materialised on the balance sheet and are therefore based on future estimates or “forecasts”. Considering the entire timeline of a cash-flow transaction, the time horizon of the forecast period is typically much longer than that of the balance sheet period. Therefore the forecast period is subject to significantly more market volatility. However, in spite of the higher risk, many companies do not regularly measure their forecast exposures. Even many companies that value the short-term predictability in cash-flows that hedging can deliver, do not hedge simply because it’s difficult to quantify the forecast exposure. The biggest obstacle companies face regarding FX management is quantifying their forecasted cash flows, especially companies with decentralised profit centers all over the world.

Even the best accounting systems rarely contain reliable, current forecasted cash flows of its global subsidiaries. Most companies perform forecasts and budgets at least on an annual basis, but very rarely getting down to the details of each currency. In order to gather reliable and current forecasts, you need to reach out to the individual financial controller at the subsidiary locations. They generally are in the best position to provide reliable forecasts beyond the current quarter.

After collecting forecasts from around the world, consolidating these exposures is the next challenge. One needs to be careful to net off naturally offsetting exposures to avoid over-estimating exposures. For example, a Japanese yen functional subsidiary selling in sterling pounds naturally offsets Japanese yen sales by a sterling functional subsidiary. Considering this analysis is to be performed over different forecast periods, it becomes apparent that without strong procedures and solid systems, the sheer amount of data to consolidate and analyse would be too vast to efficiently process.

Once the forecasted exposures are identified, you can choose to hedge them or at least understand your company’s sensitivity to market movements. If your objective is to reduce risk over a discrete period of time, for example, a budget period, then implementing a stream of hedges for the entire fiscal year is probably ideal. More commonly, companies strive to smooth volatility on an ongoing basis by layering on new hedge contracts on a rolling basis, every quarter or so, as new forecasts become available.

Administratively forecast hedging is more cumbersome than balance sheet hedging, not only in calculating the exposure, but also because accounting for cash-flow hedge contracts can be complex. In order to qualify for hedge accounting where hedge gains/losses are deferred to equity until the underlying sale or purchase hits the income statement, one must comply with up-front designation documentation and ongoing effectiveness testing. In spite of the hurdles, cash flow hedging – when there are material foreign currency cash-flows – is considered a best practice in treasury departments around the world.

Add earnings translation exposure to your analysis

In addition to transaction exposure, treasurers are also getting renewed pressure to consider the company’s earnings translation exposure. U.S. companies have suffered tremendous stress on their foreign earnings as the US dollar has strengthened. U.S. company foreign sales represent between 40% and 50% of the S&P 500. This means that even if foreign operations perform in line or better than expectation, the translation of earnings in US dollar terms will represent a lower amount than forecasted.

Accounting rules do not allow hedge accounting treatment on direct hedges of foreign earnings. Therefore companies wanting to hedge earnings translation exposure often do so indirectly. A common approach is to strategically find and hedge intercompany cash-flows that match the particular earnings translation exposure. Of course this may not be practical for every earnings exposure. Practical solutions for hedging earnings are limited, but it is nonetheless essential to quantify the exposure so you understand their sensitivity to currency fluctuations.

Regardless of hedging strategy, treasurers must understand exposures

Foreign currency risk is one of the most important risks treasurers manage. Volatile markets tend to bring about even more visibility—and pressure—to treasury departments. Foreign exchange policies and procedures may be challenged. Questions will be asked about the P&L impact of market movements. Treasurers can answer these questions and effectively evaluate the company’s foreign exchange management strategy only after thoroughly evaluating the underlying exposures, both transactional and translational.

By Kim Chase and Marc Vandiepenbeeck

Kim is a managing partner at Whitewater Analytics and also a treasury practitioner with over 20 years of experience with large, multinational corporations. Marc is a managing partner at Whitewater Analytics as well as a treasury practitioner with over 15 years of experience in international corporate finance. He has worked in public accounting, business development, global markets and corporate treasuries. Kim and Marc founded Whitewater Analytics after spending years using spreadsheets and emails to manage foreign currency exposure for Fortune 500 companies.